![]()

Crash Opportunities, Part Two

By Paul Lamont

September 29, 2008

In part one of this series, we addressed a few speculative investments that might rise over the next few years. We would like to stress that most assets will fall in a deflationary environment. We have therefore focused on preserving portfolios with U.S. Treasury Bills held at more secure financial institutions.

Preserve what you have, because when the housing market lands with a thud, the bargains will be there. For instance, one quarter of the land in Mississippi went to auction in one day during the Great Depression according to Ken Burns. We now turn to markets that we see as compelling at the bottom.

The Yellow Brick Road

As we mentioned in January, “During the period from 1980-2000, Gold experienced a bear market. As you can see from the chart below, after the parabolic rise that ended in 1980, the gold price fell for 20 years.” Markets that have been completely ignored for two decades interest us. After a 20 year bear market, gold has recently done very well.

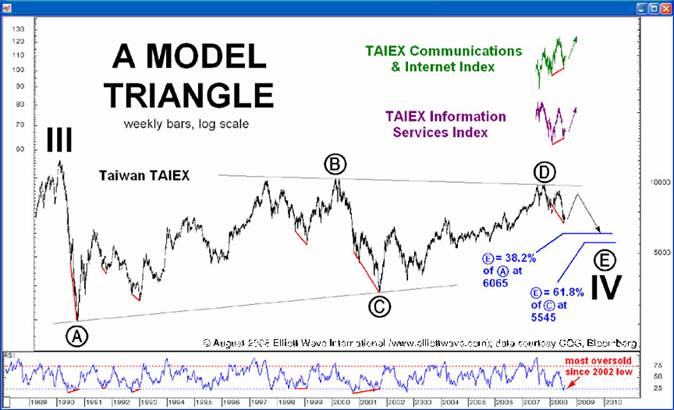

If you look at the chart below, the Taiwan stock market has been in a correction since 1990. The Japanese stock market has also experienced the same fate. We expect both of these markets to bounce in 2009 but sell-off again with the global markets into late 2010. From this twenty year bottom, we expect these two markets to perform very well.

To be considered ‘buys,’ we would like to see a torrent of horrible news coming from these countries. We would also like to see investors finally giving up on their stocks (i.e. 1979’s major news publications declaring the death of equities or 1988’s individual investors avoiding stocks as if they are poison, etc.). While the mood is currently sour, investors are not selling. When investors finally give up at the bottom and sell, we will recommend buying.

{kind=link}

The chart below shows a longer

view for Taiwan.

Jim Rogers and Marc Faber

We couldn’t discuss investing in Asia without mentioning the ‘Statler and Waldorf’ of the investment world. Jim Rogers recently stated: "We'll see if it's an overlooked trade or not. I haven't heard many people talking about Taiwan in 15 to 18 years." Dr. Faber also relates in a recent Bloomberg video that he is looking at Japan as well. We hope these two curmudgeons retire soon.

Bailouts and Government Takeovers – Why They Make Us More Bearish

As we stated in July for our subscribers, when addressing the Fannie Mae/Freddie Mac situation;

“Of course, the government is going to print. But like an adjustable rate mortgage, the government’s borrowing rate (bond yield) will jump dramatically. We discussed this outlook at the beginning of this year… As we stated last February, “As a general rule, government policy/central planning produces the opposite effect intended.”

The Treasury acceptance of mortgages does not lower risk. It transfers the risk from private hands to the public. But it does something even more destructive to the credit system. Instead it lifts rates on all credit, because all credit items are priced in addition to the ‘risk-free’ Treasury yield. So instead of propping up the housing market, the government is helping to destroy all credit markets. Government meddling was instrumental in the 1930s. We recommend reading Chapters 8-12 of Murray Rothbard’s America’s Great Depression. If Austrian economists can predict a Great Depression, then perhaps they are worth listening to when it comes to providing a solution to this mess.

FDIC Payouts Also Push Up Rates

We were under the assumption that the FDIC deposit insurance fund actually existed as a separate entry on the balance sheet of the Treasury. We were mistaken. According to a report by William Isaac, a former chairman of the FDIC, the FDIC fund was rolled into the general fund during the Johnson Administration. This means that the U.S. government will be forced to borrow money to cover bank depositors. This borrowing will only increase long term rates, thereby creating more problems in the mortgage market, which will cause more bank failures. More so than in January, it is becoming more apparent that this recession is likely to turn into a depression.

What’s Next

Reports that state if the bailout does not pass, the ‘U.S. will crash’ are ridiculous. We should just pass legislation to decree that everyone will be rich. Easy enough. We expect the U.S. Treasury’s description of a 1929-style sell-off to occur regardless of actions in Washington. We may have reached the ‘line in the sand’ described last March. More bank failures should also be expected. Banking holidays will only add to the panic. Recent gas shortages here in the South have provided us with a dry run for the reaction to bank closures.

"It's like ants to a picnic and they feed until it's all gone," - Tom Crosby, AAA.

If you would like more information

on our services, please see our recent Protect Your

Funds Now Redux. This is one of those instances when making it through the

storm is good enough.

At Lamont Trading Advisors, we provide wealth preservation strategies for our clients. For more information, contact us. Our monthly Investment Analysis Report requires a subscription fee of $40 a month. Current subscribers are allowed to freely distribute this report with proper attribution.

***No graph, chart, formula or other device offered can in and of itself be used to make trading decisions. This newsletter should not be construed as personal investment advice. It is for informational purposes only.

Copyright ©2008 Lamont Trading Advisors, Inc. Paul J. Lamont is President of Lamont Trading Advisors, Inc., a registered investment advisor in the State of Alabama. Persons in states outside of Alabama should be aware that we are relying on de minimis contact rules within their respective home state. For more information about our firm visit www.LTAdvisors.net, or to receive a copy of our disclosure form ADV, please email us at advrequest@ltadvisors.net, or call (256) 850-4161.